Challenges are a way of life for the self-employed, but when it comes to retirement, even self-employed people want to know that there’s a chance they may someday get to put away their tools. Although they’re still not in wide use, self-employed retirement plans were made possible by legislation sponsored by New York Congressman Eugene Keogh and passed into law in 1962.

Although you can still open an old-fashioned Keogh plan at some institutions, if you’re just starting out with a self-employed retirement plan it pays to choose something easier to manage. These three plans are perfect for any self-employed person who wants a simple retirement option:

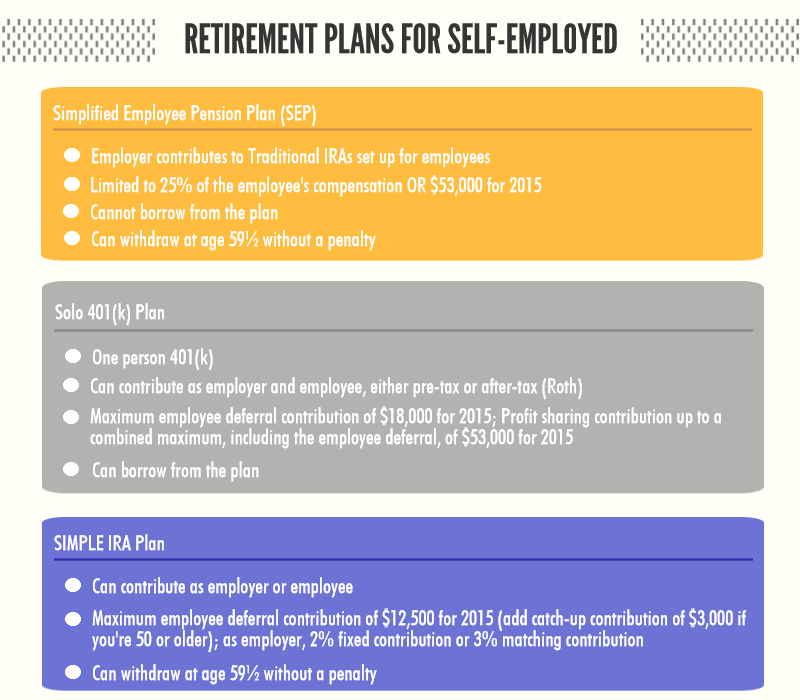

Simplified Employee Pension (SEP). SEPs are a form of traditional IRA that are great for self-employed individuals with no employees. Since the account is limited to employer contributions and each employee must receive the same percentage of their pay in their accounts, SEPs can get costly if you have even a small staff.

Your contribution is limited to the lesser of 25 percent of your net income from self-employment or $53,000 for 2015. Although you can contribute money at any time, most people wait until they file their taxes, since there are penalties for contributing too much. You can’t borrow against an SEP, but may withdraw the money at age 59½ without a penalty.

Solo 401(k). You may not know it, but you absolutely can participate in a 401(k) program for one! Commonly known as solo 401(k)s, these single person 401(k)s are identical to a 401(k) you’d receive as a benefit from an employer, minus the employer contribution matching program.

A solo 401(k) is a little tricky in the wording, since contributions are divided into employer and employee portions, but the end result is that you can give your 401(k) up to $53,000. The paperwork will be more challenging because of your dual role as employer and employee, but the fees will be fairly low and you can usually borrow against your savings in a pinch.

Savings Incentive Match Plan for Employees (SIMPLE IRA Plan). If you’re looking for something easy to be your first retirement fund, it doesn’t get more simple than a SIMPLE IRA. You can use this one with your employees, provided you don’t have more than 100 of them. It allows for both employer and employee contributions, but must be the only retirement account an individual contributor has opened for them to participate.

Unlike other self-employed retirement funds, the SIMPLE IRA requires a yearly contribution from your company of either two percent of your yearly net income or up to a three percent employer match. As a self-employed person, you can contribute up to $12,500 on your own behalf, plus the required employer contribution mentioned above on your income up to $265,000.

Self-Employed People Have Retirement Options

It’s a common and pervasive myth that being self-employed means having to rely on a spouse or non-retirement savings accounts for retirement income. That’s just not so. In fact, self-employed people have almost as many options as those employed by others. Even though you’ll miss out on the employer match contributions a 401(k) could provide, you’ll still do well with an SEP, solo 401(k) or SIMPLE IRA.

Each of these products is designed with you in mind — and that’s great news when so many other types of benefits available to traditionally employed people are difficult to implement. By starting a simple to administer and inexpensive retirement fund, you can be certain that you’ll be able to continue in the lifestyle you’re leading now well beyond the day you close shop.